![]()

Useful WebSites:

April 1999

July 2000

November 2000

December 2000

January 2001

February 2001

March 2001

April 2001

May 2001

June 2001

July 2001

August 2001

September 2001

October 2001

November 2001

December 2001

January 2002

February 2002

March 2002

April 2002

May 2002

June 2002

July 2002

August 2002

September 2002

October 2002

November 2002

December 2002

January 2003

February 2003

March 2003

April 2003

May 2003

June 2003

July 2003

August 2003

September 2003

October 2003

November 2003

December 2003

January 2004

February 2004

March 2004

April 2004

May 2004

June 2004

July 2004

August 2004

September 2004

October 2004

November 2004

December 2004

January 2005

February 2005

March 2005

April 2005

May 2005

June 2005

July 2005

August 2005

September 2005

October 2005

November 2005

December 2005

January 2006

February 2006

March 2006

April 2006

May 2006

June 2006

July 2006

August 2006

September 2006

October 2006

November 2006

December 2006

January 2007

February 2007

March 2007

April 2007

May 2007

June 2007

July 2007

August 2007

September 2007

October 2007

November 2007

December 2007

January 2008

February 2008

March 2008

April 2008

May 2008

June 2008

July 2008

August 2008

September 2008

October 2008

November 2008

December 2008

January 2009

February 2009

March 2009

April 2009

May 2009

June 2009

July 2009

August 2009

September 2009

October 2009

November 2009

December 2009

January 2010

February 2010

March 2010

From a recent Photoshop contest at Worth1000.com:

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/31/2007 07:30:00 PM Send this post:

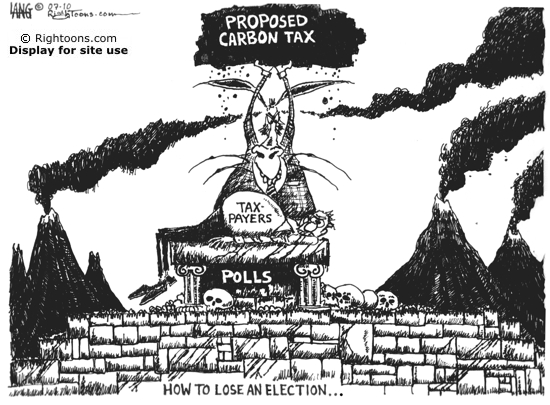

Cause & Effect...

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/31/2007 06:47:00 PM Send this post:

Coming Hike. Expiring tax relief, big spending on the agenda for Congress. – Our GOP don’t have much time left to extend the Bush tax cuts before they expire.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/30/2007 12:02:00 PM Send this post:

Sales Tax Holidays

The most recent email newsletter from TaxCoach Software had a link to this handy listing of the various sales tax free days in many states around the country.

Be sure to click on the link to your state’s specific website; because there are several exceptions. For example, I noticed that there’s nothing listed for here in Arkansas; but I could go up into Missouri next week and avoid sales tax on up to $3,500 of computer hardware. However, it seems that most cities and counties aren’t participating in this “holiday;” so only the state portion of the sales tax will be waived.

Labels: SalesTax

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/26/2007 05:10:00 PM Send this post:

5 mistakes that can tax your 401(k) – From USA Today

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/20/2007 01:28:00 PM Send this post:

Outdated Info

A week or so ago, I stumbled across a web site for a group in Oregon called The Settlement Institute that claims to have better solutions for reducing capital gains taxes than just normal 1031 exchanges. They sell a book for $29.97 with supposedly the top nine ways to sell properties and businesses that they claim even CPAs and tax pros don’t know. They even have an affiliate program costing $297 up front and $99 per year that is supposed to allow tax and financial advisors an opportunity to earn referral fees for steering clients their way to some kind of vague and unexplained installment sale scheme.

As part of my never ending ongoing research into tax issues, I signed up for their free email newsletter and downloaded their free pdf booklet on “5 Steps to the Right Exit Strategy” which was far too vague and useless to be of any value. I’m now receiving daily hard-sell emails for their services. The one I received today was amazing in its inaccuracy. I have copied and pasted it exactly below. See if you have the same reaction as I did when reading it.

Subject: Kerry, roll over the gains on your primary residence?Hi Kerry,I know that you have probably heard of a 1031 exchange and a IRA rollover, but did you know that you can actually "roll over" the capital gains on your primary residence and defer your capital gains taxes for a long time?Well... most people don't!This tax loophole is not one of the more commonly used loopholes, simply because people do not know about it and their situation just does not call for its use.Let me tell you how it works very briefly.The 1031 exchange has a bit of a black hole when it comes to your primary residence. It doesn't work all that well.However, you can do pretty much the same thing with your primary residence with the "roll over" loophole.To utilize this loophole all that you have to do is keep on "trading up" to a home of equal or greater value. As you keep "trading up", the rolled over capital gains accumulate until you finally decide to downsize to a lesser valued home.To make this even nicer, at the age of 65 you get a lifetime exemption of $125,000 (as of 2007). So, if you keep "rolling over" and do not downsize until you reach 65, you get to take the $125,000 exemption on your capital gains. This is in addition to any "one time" exemption that you already get ($250,000 if unmarried: $500,000 if married).This is a nice little gift from Congress that rewards people who keep upgrading to higher value homes over the years.Kerry, if this loophole helps you out a bit, congratulations!My best,-JLMP.S. - This is just one tip of hundreds that are in our comprehensive manual, "The Top 9 Ways to Sell...". You can download this manual at:The Settlement Institute18414 Old River Landing

Lake Oswego, OR

97034

US

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/20/2007 11:02:00 AM Send this post:

You have to be really desperate for cash to scrounge through your dog’s droppings looking for some that made it all the way through. These people in Wisconsin were that desperate. Their dog ate almost $750 and the owners recovered about $400.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/19/2007 09:15:00 PM Send this post:

Section 179 For Recording Equipment?

Q:

Subject: Sect 179 Question

Kerry,I found your website while Googling the topic of Sect 179 first-year deductions. I would like to ask your opinion about a specific piece of electronic equipment and it's eligibility for first year deduction as opposed to depreciation.I am a self-employed Human Resource Training & Development Consultant. My business is an LLC and I report income via K-1. I have recently purchased a 16-track (portable) digital recording studio, along with several peripherials (external CD-R / headphones / condensor microphone / mic stand / mic cable), all totaling about $800. The intent of this purchase is to be able to record some of my training session content to CD for the purpose of what trainers often call "back of the room" sales - CD's available for sale on-site to participants in my training sessions, or perhaps available for purchase through my website.Under this scenario, I believe all of these items are deductable under the provisions of Sect 179 for first-year full cost deduction. I would like to know if you concur?Thanks in advance for any reply you may be kind enough to offer.

Thanks and have a GREAT day!

More Info Requested:

I need more info on your situation in order to answer your question.

You said the business uses K-1s. Is it a 1065 or 1120S?

How many owners of your business?

Did you buy the equipment through the business or personally?

What has your personal professional tax advisor said about this?

Kerry Kerstetter

More Details:

Sorry for not being more specific, Kerry. The busniess is owned by my wife and I with no additional partners. We do report income using 1065's. The equipment was purchased with business funds directly - not personal funds with reimbursement through business funds. My wife is also our accountant (she has an accounting degree but is not a CPA). She is very knowledgable about busniess tax issues but is a bit hesitant to fully expense these items for the 2007 tax year as opposed to depreciating them over some reasonable life span. I believe they qualify for full cost purchase year deduction. Thanks again for your reply.

Thanks and have a GREAT day!

A:

Thanks for the additional info. I was worried that you may have been trying to use a 1065 for a single member LLC, which is not legal to do. It's fine with a multi-member LLC.

I don't see any reason why the equipment wouldn't qualify for the Section 179 expensing election. However, whether you can actually claim any deduction is a different issue. I forgot to ask whether the LLC is profitable or not, but that factor will decide whether any 179 will be allowable for the year. As you can see on my web page explaining the Section 179 deduction, there has to be enough net income from the business before that expense in order to be able to claim it. In other words, the Section 179 deduction cannot add to or create a net loss. If this income limitation will disallow the Section 179, you may very well be better off just claiming the normal depreciation expense, which can add to or create a net loss.

This is the kind of thing that you should have consulted with a professional tax advisor prior to the purchase rather than after. If you had purchased the equipment in your individual name instead of the LLC's, there is a much greater possibility that you would be entitled to a larger net Section 179 deduction because the taxable income test at that level will include other sources of earned income, such as W-2s and other Schedule C income.

I mean no offense to your wife, but even with her accounting knowledge, you need to have a working relationship with a professional tax advisor who can fill in the gaps. Over the years, I have had several clients who were CPAs and professional accountants who paid me to give advice, review their work and even to prepare their tax returns because they were aware of their own limitations. A similar relationship would be helpful for you and your wife to establish with a professional tax advisor, who could very easily have gone over the pros and cons of buying the new equipment in your personal name versus the LLC's name. Similar issues will definitely be popping up all the time, so the sooner you start working with a tax pro, the better prepared you will be.

Good luck. I hope this helps.

Kerry Kerstetter

Follow-Up:

Thanks again for your replies. All good advice and very understandable.

Thanks and have a GREAT day!

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/19/2007 06:11:00 PM Send this post:

Buying A Large Vehicle

Q-1:

Subject: More 179 Questions

Hi,I see that you regularly advise people to ask your "tax professional". Mine doesn't seem to be able to give me an answer that gives me a "warm and fuzzy feeling" that he knows what he's taking about on this subject. Where can I find specific IRS info on which SUVs are on the list of s179 approved vehicles? What section of the IRS code addresses whether on not the SUV must be new or can be used? And, most importantly, does the vehicle have to be registered to his company in order to be uses as a small business writeoff or can it be registered in his name as President of the company and be used for the writeoff?My husband refuses to make a purchase until be can get a verifiable answer and I want my new Escalade.Thanks in advance for any advice.PS. Can you recommend a Financial Planner/Tax Advisor in the eastern Long Island area of New York.

A-1:

IRS doesn't certify vehicles for Section 179. The definition of luxury vehicles that are severely restricted in their depreciation and Section 179 deductions was defined in 1984 to only include vehicles of less than 6,000 pounds gross vehicle weight. Check the stats on the vehicle you are considering purchasing to see if that particular model is heavy enough.

I had put together some links to some lists of the most popular vehicles weighing more than 6,000 pounds; but many of those links have gone out of service.

Assets qualifying for Section 179 do not have to be brand new; just new to you. This is all explained on my website.

If you are unincorporated, the actual title on the vehicle isn't as important as the number of business miles driven compared to the total miles for the year.

You definitely need to be working with a good tax advisor. As I mention in my tips on selecting one, basing that decision simply on geographic concerns is the wrong way to make that choice.

I do have some names of other tax pros, including one in Brooklyn, on my website.

I hope this helps. Good luck.

Kerry Kerstetter

Q-2:

Hi Kerry,Thanks for your reply.We have a Sub S Corporation. What are the title ramifications of that? From what I can gather the vehicle has to be between 6,000 and 14,000 lbs. GVW I plan to buy an Escalade which is surely on the list as it is well above 6000 lbs. GVW We plan to register it in my husbands name as he is 100% Owner of the corporation and hopefully we will be able to take the Small Business Luxury Vehicle writeoff of $25,000 + $5,000 the first year. Comment?

A-2:

This is a perfect example of why it is so important to be working with a tax pro because there are a number of different ways in which to handle a large vehicle purchase.

I'm assuming that it will be used at least 50% for business or else no Section 179 would even be possible.

Following are just a few of the variations that need to be reviewed with your own personal professional tax advisor.

If the vehicle's title is in your and/or your husband's personal name, there is a high likelihood that the actual net tax savings from the Section 179 and depreciation deductions won't be as much as with corporate ownership because you would have to show them on Schedule A as Unreimbursed Employee Business Expenses. For several reasons, Schedule A deductions are not as powerful as are deductions that reduce AGI on the front of the 1040.

If the corp owns the vehicle, the Section 179 will pass through to your Schedule E via the S corp's K-1 and will reduce your AGI, resulting in a larger net tax savings than on Sch. A.

One additional twist to the corp ownership scenario is how you account for non-business personal usage of the vehicle. You need to work with your personal professional tax advisor to set up a policy to either reimburse the corp for that usage or include its value as additional W-2 income.

Also, you may be confused on the weight issue of vehicles qualifying for the large Section 179 deduction,. Those weighing between 6,000 and 14,000 pounds are eligible for up to $25,000 of Section 179. Those weighing more than 14,000 pounds are eligible for as much as the full $125,000 annual overall limit.

Good luck. I hope this helps.

Kerry Kerstetter

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/19/2007 05:09:00 PM Send this post:

Labels: comix

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/16/2007 04:55:00 PM Send this post:

Soaking the evil rich...

Dems grapple with ‘rich’ – A cornerstone of DemonRat tax policy has always been classic Marxism by sticking it to those folks that they declare to be the “evil rich.” This article is another illustration of how flexible that term is. As I’ve been describing for decades, there are literally dozens of penalties on the evil rich built into the tax system that each start at different levels of income, and more are obviously being planned. When the Clintons move back into the White House, we can at least be sure of seeing another new tax like their 1993 “millionaire surtax” that kicked in at taxable income of $250,000.

As destructive as such penalties on success are for the economy and capitalism in general, they will be great for those of us in the tax minimization profession as we help more clients use such techniques as income shifting and multiple entities to avoid these new attacks on their wealth.

Labels: Commies

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/14/2007 09:34:00 PM Send this post:

How kids learn about taxes...

(Click on image for full size)

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/14/2007 08:05:00 PM Send this post:

DemonRat plan to sabotage the economy...

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/13/2007 06:08:00 PM Send this post:

California's asset grab – You know the rulers in Sacramento have gone too far when even the left-leaning LA Times writes an editorial opposing the PRC’s plans to outright steal assets from people as a budget balancing technique.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/10/2007 09:49:00 PM Send this post:

Sisyphus in the Senate – A very appropriate analogy by George Will for the task of our rulers ever actually simplifying taxes.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/10/2007 09:17:00 PM Send this post:

What's erotic to accountants?

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/10/2007 05:58:00 PM Send this post:

Is a 1031 exchange needed?

Q:

My parents are both deceased and I am presently under contract to sell the farm. I have made my intention to perform a 1031 exchange known to the potential purchaser.

I would like for you to advise me on the best course of action involving this matter. My desire is to reinvest the portion of the sale which would be subject to capital gains tax.

As a brief history; the farm was purchased in 1995, my mother died in May 2002, my father in November 2003.

I have always lived here since 1995.

I don't know how to establish the new value basis for the farm or how the exemption on the sale of my primary residence will affect my overall tax liability.

The purchase price will be substantially more than average requiring, I believe, an exchange to avoid capital gains tax.

As it stands now the closing date could be anywhere from September of this year to February of next year. An investment group is purchasing the farm and other adjacent properties for a commercial venture and there are certain contingencies which make it impossible to know the exact closing date.

So I basically need to know where I stand so I will be prepared if the sale concludes as expected.Sincerely:

A:

It's critical that you consult with a professional tax advisor because there are a number of issues that need to be considered.

First is the determination of your cost basis in the property in order to determine how much potential profit you would be looking at with a sale. This depends on how you acquired legal title to the property, which wasn't clear in your email. The three most common ways to acquire title would be by purchase, gift or inheritance. Each one gives a very different cost basis amount.

For example, if you purchased it from them while they were alive, that would be your cost, plus improvements and less depreciation.

On the other hand, if they gifted the property to you while they were alive, their cost basis carries over to you even though Gift Tax returns are based on the property's fair market value at the time of the gift. If you received the property as a gift, you would start with their adjusted cost basis and add in any capital improvements and subtract any depreciation you have claimed to arrive at your current cost basis.

Finally. if the title to the property was transferred to you as a result of your parents' death, your cost basis in it would be its fair market value as of the date they passed away, or an alternative date (usually six months later) if that was used on their estate tax return.

If you did inherit the property, with the cost basis being established based on its value in 2003, your potential gain shouldn't be as high as it would be if you had purchased the property or received it as a gift.

The other big issue that you need to work on with a professional tax advisor is how much of the property qualifies as your primary residence so that the sale price can be properly allocated between it and the farm portion. As you probably know, up to $250,000 of gain from the sale of a primary residence is tax free; $500,000 if you are married. I have a full explanation of this extremely useful tax break on my website.

I hope these points are useful in deciding if you have a tax problem to worry about, in which case a 1031 exchange would be a wise move.

Kerry Kerstetter

Labels: 1031

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/09/2007 07:40:00 PM Send this post:

LifeTime Gift Tax Exclusion

Q:

Subject: gift tax question

My mother will be selling property soon that I was supposed to inherit upon her death. I am supposed to receive the proceeds, but instead of her gifting me the property, I have been advised that she should sell the property in her name to pay lower capital gains rates and alternative minimum taxes than I would since my annual income is much higher and gift the after capital gains tax proceeds to me.

I was told that she could give a one time gift of up to $1,000,000 exempt from gift tax but subtracted from her eventual estate. In other words, for 2007 the gift of $1,000,000 would reduce her exempt estate taxes to $1,000,000 from the $2,000,000 current limit. I have been assured by my CPA that is the case, but I can find nothing online including IRS.gov that mentions anything other than a $12,000 annual exemption from gift taxes.This deal is based on my ability to receive the after tax proceeds (approx. $850K) without any gift taxes being paid by my mother in addition to the capital gains taxes. If both capital gains taxes and gift taxes applied to these funds the government would end up with more of the proceeds than we would. I appreciate any advice you can share.

A:

You need to check IRS Publication 950. It explicitly mentions the lifetime exclusion of $1,000,000.

Here is a link to that part on the web.

To see the entire Pub. 950:Web-Friendly HTMLGood luck.

Downloadable PDF

Kerry Kerstetter

Labels: Gifting

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/09/2007 07:22:00 PM Send this post:

No Change In SUV Section 179 Limits

Q:

Subject: section 179 for SUVIn 2007 do you know if you can still expense $25000 of a vehicle with GVW over 6000 pounds under the Small Business and Work Opportunity Tax Act of 2007? Thanks

A:

That rule has not been changed.

The only change in the new tax law is to raise the overall maximum Section 179 from $112,000 to $125,000 for 2007. The special $25,000 limit on SUVs was not modified.

Kerry Kerstetter

Follow-Up:

Thank you

Labels: 179

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/09/2007 07:13:00 PM Send this post:

There are never enough types of taxes to satisfy the DemonRats...

X-rated trade targeted by Calif. tax measure

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/09/2007 06:28:00 PM Send this post:

When clowns go bad...

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/07/2007 09:07:00 PM Send this post:

Intuit's Summary of New tax Law

New Tax Law Provides Breaks for Small Business

More Penalties for Tax Return Preparers

Qualifying Age for "Kiddie Tax" Goes to 23

As they often do, a handy doc file explaining the changes for clients is included that can be downloaded and sent out.

Labels: taxes

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/07/2007 02:18:00 PM Send this post:

QB Data Conversion

I recently took a survey for QuickBooks on their new Client Solution Center as part of their Certified ProAdvisor program. While I like their new data conversion tool that allows people to import data from Peachtree, Microsoft Small Business Accounting and Microsoft Office Accounting, it does have a serious limitation, which I explained as follows in the request for additional feedback.

Your conversion tool should include the ability to convert from the QB Online format to the QB desktop format. I have always advised against using your online service because of the inability to do this, and will continue to advise against your online service until it is possible to easily move data from the online program to the desktop one.

Labels: QB

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/07/2007 11:46:00 AM Send this post:

'Kiddie Tax' Loophole Is Closing! – Income shifting strategies may need to be revised if you have kids between 14 and 24.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/06/2007 09:58:00 PM Send this post:

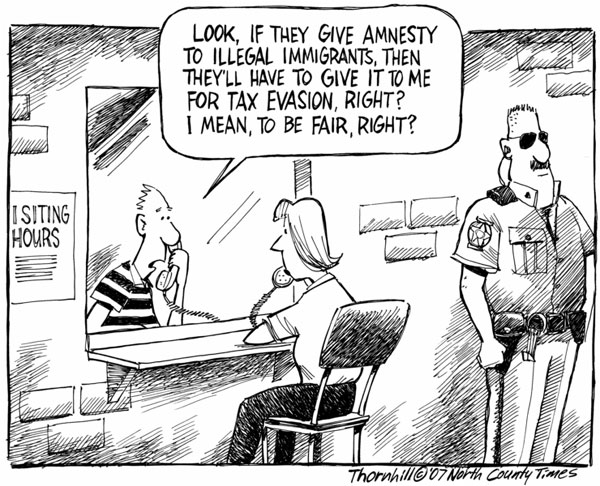

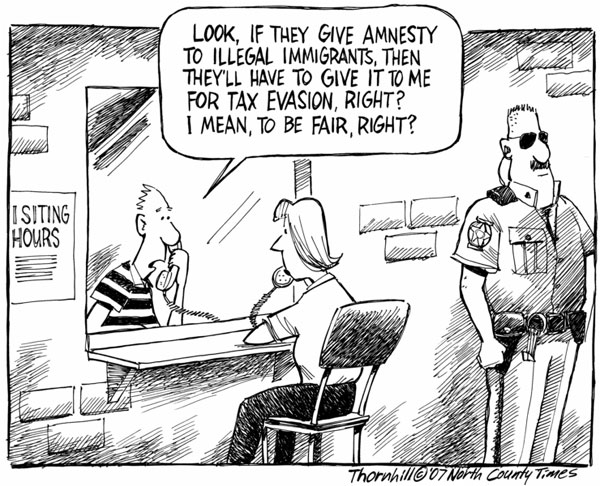

Amnesty for everyone?

Richard Hatch is jealous of Scooter Libby.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/06/2007 12:10:00 PM Send this post:

Amnesty for everyone?

Labels: comix

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/06/2007 12:10:00 PM Send this post:

A tax-free Fourth of July would fit with founders – Interesting concept, to be free from the slavery of taxation for even one day. Unfortunately, it has the same chance of happening as the proverbial snowball in Hell. Our rulers could never stomach the mere thought of their subjects tasting even the slightest amount of freedom from their tax slavery. And, as Chairman Hitlary constantly reminds us, paying high taxes is the epitome of patriotism.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/03/2007 10:43:00 AM Send this post:

IRS very focused on businesses, especially sole proprietorships

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/02/2007 05:13:00 PM Send this post:

More attacks on capitalism by the DemonRats

Hitlary Clinton’s ‘Patriotic’ Tax Hike

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/02/2007 03:03:00 PM Send this post:

Gifts Tax Free For Recipients

Q:

Subject: gift taxes

Hi,So to clarify the gift tax law.......the recipient has no tax ramifications if the gift is over the legal limit. For instance if I gift someone 12,500 they have no responsibility for any tax on that money?Thankyou,

A:

That is true in almost all cases. However, if you give someone pre-tax money, such as an IRA or other retirement account, that money will be taxable to the recipient. Every other kind of gift of after-tax money is completely free of income tax for the recipient.

However, the giver will have to file a gift tax return (709) to report gifts to any single person in any calendar year in which the total exceeds the annual exemption.

Also, be aware of the fact that gifts do not reduce the taxable income of the giver, a very common misconception that people have.

Before any large size gifting program is implemented, you should work with your personal professional tax advisor to ensure that you understand the rules and implications of what you are doing.

Good luck.

Kerry Kerstetter

Follow-Up:

thankyou

Labels: Gifting

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/01/2007 08:27:00 PM Send this post: