![]()

Useful WebSites:

April 1999

July 2000

November 2000

December 2000

January 2001

February 2001

March 2001

April 2001

May 2001

June 2001

July 2001

August 2001

September 2001

October 2001

November 2001

December 2001

January 2002

February 2002

March 2002

April 2002

May 2002

June 2002

July 2002

August 2002

September 2002

October 2002

November 2002

December 2002

January 2003

February 2003

March 2003

April 2003

May 2003

June 2003

July 2003

August 2003

September 2003

October 2003

November 2003

December 2003

January 2004

February 2004

March 2004

April 2004

May 2004

June 2004

July 2004

August 2004

September 2004

October 2004

November 2004

December 2004

January 2005

February 2005

March 2005

April 2005

May 2005

June 2005

July 2005

August 2005

September 2005

October 2005

November 2005

December 2005

January 2006

February 2006

March 2006

April 2006

May 2006

June 2006

July 2006

August 2006

September 2006

October 2006

November 2006

December 2006

January 2007

February 2007

March 2007

April 2007

May 2007

June 2007

July 2007

August 2007

September 2007

October 2007

November 2007

December 2007

January 2008

February 2008

March 2008

April 2008

May 2008

June 2008

July 2008

August 2008

September 2008

October 2008

November 2008

December 2008

January 2009

February 2009

March 2009

April 2009

May 2009

June 2009

July 2009

August 2009

September 2009

October 2009

November 2009

December 2009

January 2010

February 2010

March 2010

If Robin Hood were audited...

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/30/2007 08:43:00 PM Send this post:

Some audits are more probing than others...

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/30/2007 02:03:00 PM Send this post:

A new kind of flat tax?

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/28/2007 02:38:00 PM Send this post:

We get no respect...

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/28/2007 01:09:00 PM Send this post:

Some tax returns are works of art...

Labels: comix

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/27/2007 09:10:00 PM Send this post:

Finding new tax pro...

Q:

Dear KerryThank you very much for taking the time to send such a thoughtful response.Is there a tax professional that you might recommend in Austin, Texas?Many thanks again for taking the time to help with my questions!Kind regards,

A:

There is a Texas tax pro listed on my website.

Be sure to check out my hints on choosing a tax pro, especially the point about geographic location not being as important as other criteria.

Good luck.

Kerry Kerstetter

Follow-Up:

Thank you for the kind reply and info, Kerry!All best

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/23/2007 11:43:00 AM Send this post:

Why maximum Sec. 179 limit?

Q:

Hi Kerry,First of all I would like to thank you for the website! It's very informative and a great read. But there is something that recently came up that is driving me crazy. I hope it's ok for me asking.I run a dedicated server business which basically means I purchase rackmount servers and then you can say I rent them out to individuals and companies for a monthly fee. Now the question is regardiing the Section 179 and the actual server purchase. What the CPA has done is utilized the maximum Section 179 and then depreciated the rest. Now this provides a huge problem is many ways. First of all assuming I purchase the server for $1,000 in will take many months to recoup just the initial cost of the server not including the cost to maintain the server, power cost, etc. Now what is being proposed is that the excess of the maximum in the Section 179 is now considered "income" - taxable "income". So now this $1,000 server has become a $1,000 + tax rate server and will take even longer to break even. What is worse is let's assume the excess is $200,000, now I just spent that $200,000 to acquire the server to which the customer will go on. How in the world is it expected of me to have the taxable rate for this $200,000?So in essence we have my payroll / dividend which gets passed down to me as a normal s-corp would. Let's assume it's $100,000 so roughly with state and federal would be $40,000 tax liability. But now if you pass on the above server purchase above the Section 179 limit then I am supposed to magically find another $80,000 in tax fee?? Taking the above $200,000 which is now "income" at 40% is $80,000. So we now take the $80K and original $40K income tax which would equal $120K. Which in the end would mean I have a net of negative $20k! What in the world is going on here? I know I am missing something and hoping you can give some insight before I discuss further with CPA.Hope the above makes sense... Shouldn't the "servers" which I need just like I need the power / space to house them in be considered a "operating expense" and then none of this non-sense would happen?Thanks for your time!

A:

I'm not sure if I'm completely clear on your question. It seems to be that you are upset at not being able to fully deduct the cost of all of your new equipment in the very first year.

From a purely cash basis of running a business, that is a valid concern, especially if you pay cash for all of the new items rather than finance them with loans. That is simply a reality of running a business and something that you are going to have to learn how to deal with.

From the perspective of GAAP (generally accepted accounting principles) as well as tax law, unlimited first year expensing is not how new equipment has ever been treated on the books of businesses. There is obviously a big difference between the treatment and deductibility of operating supplies that are used up in less than one year, and items that last for several years. It has always been standard accounting practice to amortize or depreciate the cost of assets that provide service to the business over multiple years over those years as a better matching of expenses with the related revenues. This has always been the case for all kinds of businesses that buy equipment. Trucking companies and machine shops have the exact same situation that you have.

If your servers are used over more than one year, you will have to deal with this as a depreciation issue. If you have a track record of having to replace each of your servers in less than one year, you could possibly justify deducting their purchases as annual operating supplies. If you try this approach, you need to be very prepared to document the fact that none of your servers last over a year because the large numbers involved will most definitely attract IRS scrutiny. An experienced tax pro will know how to include the proper documentation with your tax return to prevent an IRS audit on this issue.

In order to encourage business owners to stick their necks out and acquire more equipment, there have been various tax incentives passed by our rulers in DC over the year. The most lucrative have been the Investment Tax Credit, which gave a rebate of 10% of the purchase price right against the taxes (repealed in the 1986 tax law) and the Section 179 expensing election, which has been raised from its earlier limit of $5,000 per year to the $128,000 we will have for 2008. The tax savings from the Section 179 deduction are designed to offset the kind of cash flow problem you alluded to in your email.

What you need to do is to work more closely with your professional tax advisor to ensure that you don't put yourself into a cash flow problem. This may entail financing some of the equipment purchases with loans in order to be able to retain some cash for other expenses, including taxes. Another strategy may be to stagger your equipment purchases so that you can maximize the annual Section 179 allowance. Buying too much in one single tax year can very easily cost you much more in taxes than you would have if you spread those purchases out over multiple years.

I hope I addressed your concerns. If I missed the point, please let me know.

Kerry Kerstetter

Follow-Up:

Kerry,Thank you for the detailed explanation and you hit it on the money. I simply was not aware that the equipment expense will be considered income when it reaches over a certain amount. Everything was paid cash so now I have to pay taxes on it, which IMO is extremely unfair. Simply I have to make purchases smarter and try to get into leases and longer term notes than paying cash.Will be certain to get this in order for 2008 so we don't encounter this problem ;-). Know that we are utilizing the section 179 to the max. Will look into the tax credit as you noted.Thanks again!

My Reply:

I'm glad I was able to help.

The Investment Tax Credit for new equipment purchases is no longer available. It was repealed in 1986. I was just explaining the history of tax incentives for new equipment purchases. The Section 179 expensing election was designed as a replacement for the ITC with the same qualifying rules.

Your personal tax advisor can give you much more details for your unique circumstances.

Good luck.

Kerry

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/23/2007 11:35:00 AM Send this post:

2008 Federal Tax Rates

Right on schedule, CCH has released their inflation adjusted calculations for the Federal individual income tax brackets and other items that are adjusted annually. When I have a chance, I will be setting up a new page on my website for these 2008 figures.

Besides the new tax bracket break points, there a few other interesting items that will be of interest to readers.

The Section 179 limit goes up to $128,000 for tax years starting in 2008.

The annual gift tax exemption will remain at $12,000 for 2008.

[Update] A new page has been added to my website for the 2008 Federal rates. I’ve also updated the Section 179 info for 2008 on its special page, as well as the Quick Reference page.

Labels: IRS

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/20/2007 11:19:00 AM Send this post:

Special IRS Web Section Unveiled for Homeowners Who Lose Homes; Foreclosure Tax Relief Available to Many - Here is a direct link to the IRS FAQ page on foreclosures.

As I’ve said before, this entire issue is being blown way out of proportion in regard to its negative tax consequences. Most people who suffer foreclosures will either have nondeductible losses or be more than covered by the Section 121 tax free exclusion.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/19/2007 09:59:00 PM Send this post:

Upcoming tax hikes?

Congress’s Middle-Manager Tax Hike – Just one more example of how our imperial rulers in DC have no qualms about changing the rules on retirement plans after the fact, just to screw the evil rich folks. Are Roth IRAs next?

Taxed to Death – With Chairman Hitlary openly extolling the virtues of communism on the campaign trail, the odds of one of the main planks of her beloved Communist Manifesto - the estate tax - being eliminated, are slimmer than ever.

Labels: TaxHikes

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/19/2007 12:50:00 PM Send this post:

Losing Roth IRA tax break?

Q:

Subject: Fair Tax & Roth accounts?

How is the Fair Tax supposed to integrate with Roth accounts? These are *supposed* to be tax-free upon withdrawal. The Fair Tax represents a very large stealth tax increase on these accounts.

A:

There's no way to make such a radical change in the tax system without also affecting the results of tax motivated transactions.

This is why I have always been critical of plans by people to convert conventional IRAs to Roths. Paying real tax money now for promised tax savings down the road has never felt like a good idea because there is no guarantee that the tax free aspect will survive the whims of our rulers in DC. While I do support the concept of the FairTax, I'm not as worried about it messing up Roth IRAs as I am about our rulers instituting a means test for taxation of Roth IRA income in the same way they did for Social Security recipients.

Thanks for writing.

Kerry Kerstetter

Follow-Up:

I did it because (a) I had relatively low tax cost since I converted during a year when I was unemployed, and (b) I won't be making any more contributions to the account. You're right about their tendency to take away what they have given when their lack of restraint catches up to them. I shudder at the thought of Hilary as President and a Democrat-majority Congress.A means test? That would be horrible! Of course, that wouldn't raise the kind of revenue the IRS expects. The means test only screws middle-income taxpayers. Low income (though with non-indexed income thresholds this becomes progressively less meaningful) people won't be affected, assuming they even have a Roth account, and people with plenty of non-Roth income won't have to take distributions. To give means testing real sharp teeth you'd need to make Roth IRAs subject to RMD.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/18/2007 10:14:00 PM Send this post:

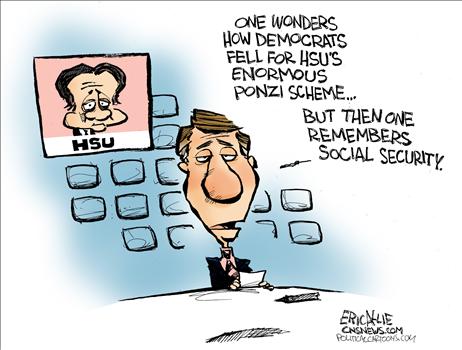

Who serves whom?

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/18/2007 09:16:00 PM Send this post:

(Click on image for full size)

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/17/2007 11:15:00 PM Send this post:

Labels: Accounting, comix

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/16/2007 09:03:00 PM Send this post:

No one size fits all...

Q:

Subject: S vs. C orp

Do you still reccommend an S corp for a 1099 contact sales rep for surgical device sales .I am starting out fresh and will recieve $75k first year and scale up to 200 K by end of year 3.Thanks,

A:

You must have me mistaken with someone else because I have never made any kind of blanket endorsement of the use of S corps. I always warn that there is no such thing as a one size fits all approach and that you must work with an experienced tax professional in order to determine what is best for your unique circumstances.

I do have some comparisons of C and S corps on my website, but these are no substitute for the experience and judgment of a tax professional. Start working with one right away before you head any further in the wrong direction.

Good luck.

Kerry Kerstetter

Labels: corp

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/15/2007 07:50:00 PM Send this post:

No Homework Questions Accepted...

Q:

Subject: questions

Saw your website and have a few questions. I have gone back to school and have an assignment on the various types of businesses and their associated negative or positive ramifications on each one. Do you have a second to chat?

A:

I'm sorry, but it has always been my policy to not answer homework questions.

I barely have any time to answer real world questions.

Good luck.

Kerry Kerstetter

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/15/2007 07:39:00 PM Send this post:

State tax home is critical...

Q:

Subject: State tax question

Hello KMK,

Tax Guru is a neat website. Compliments!I am an Illinois accountant with a client with an Illinois S-corporation, but who lives in California. With the lower Illinois individual income tax rate, I would like to have Illinois tax the S-corporation income, and leave it off of the California individual return. Do you know how to do this in the California return?If you do "out-sourced" tax research for others, please let's discuss your charges for the service. Thoughtful research is appreciated.

A:

It will all depend on which state is your client's official tax home. If it's California, he will have to report all income from all sources (including the IL 1120S) on his Calif. 540. Of course, he will also need to file a nonresident IL return. He will be able to claim a credit against his CA taxes for part or all of the IL tax on that income. As you know, the net effect of the out of state tax credit is that he ends up paying the higher of the two states' taxes.

If your client can establish his official tax home in IL or another state, he can file a 540-NR as a CA part year or nonresident and then only allocate his CA source income to that state. Many people use tax free states, such as Washington, Nevada, Texas, or Florida, as their official tax home for just this reason.

I hope this helps. I'm still not caught up enough with the workload with my current paying clients to be able to accept any new ones. General questions that should be of interest to my blog readers are always welcome however.

Good luck.

Kerry Kerstetter

Follow-Up:

Thank you for your prompt reply, and good advice.

Labels: StateTaxes

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/15/2007 07:32:00 PM Send this post:

Fear of the FairTax – Neal Boortz takes on Bruce Bartlett’s attacks against the FairTax.

Labels: FairTax

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/13/2007 09:59:00 PM Send this post:

How to kill economic growth...

For anyone who thinks I am overly paranoid about the future of special tax rates for long term capital gains, check out this prediction of DemonRat plans, including raising the current 15% rate to 35%.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/12/2007 01:06:00 PM Send this post:

Tax free capital gains?

Q:

I have read that the long term capital gains tax will be zero for the year 2008. Is this true? If so I may delay selling my remodeled house until next year. Please advise.

A:

It is true that there is a Federal tax reduction on long term capital gains scheduled for sales in 2008, 2009 and 2010 under current tax law. This could very easily be repealed, possibly retroactively, if the DemonRats have their way; so there is no guarantee that anyone will actually be able to benefit from this.

Assuming our rulers can keep their hands off of this tax break, the actual size of the benefits is still very limited. As with all tax matters, the reality of its application is much more complicated than we all wish.

Under current Federal tax law, people with long term capital gains that would normally be in the 10% or 15% bracket only have to pay 5% Federal tax on just that portion of the gain in those lower brackets. The portion of the gains that push the taxable income into the higher brackets is taxed at 15%. You can see the 2007 brackets on my website. The 2008 inflation adjusted Federal brackets should be released in a few weeks.

Now for the special tax break. For sales in 2008, 2009 and 2010, that portion of long term capital gains that would otherwise be subject to a 5% Federal tax rate will have a zero Federal tax rate. The portion of the gain above the 15% bracket will still be subject to a 15% rate. In addition, depreciation recapture is not considered to be a capital gain and it will still be subject to a 25% Federal tax rate. State taxes will also still be applicable on the full gains; so the overall tax savings may be relatively minor, especially for the sale of highly depreciated property, such as rental homes. As Sherry mentioned earlier, 1031 exchanges will still be a very important tool for real estate investors wishing to minimize their taxes.

I hope this isn't too confusing; but out imperial rulers in DC seem to like to keep the rules as muddy as possible.

Let me know if you have any more detailed questions.

Kerry

Labels: CapGains

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/11/2007 12:27:00 PM Send this post:

Estate Asset Transfers

Q:

Subject: Estate Taxes

My wife died with a will that basically leaves everything to me. Two houses were right of survivor, One CD she owned alone that was pod. Both of her iras were also pod. The only thing she had in her name alone that wasn't pod or ros was stock valued at about $13K. The total value of the above was about 700K. My attorney says that I can pass any amount of the above to our two children without any tax consequences. It seems strange that the amount is an option. I want to pass along to them as much as I can afford without putting myself in a cash bind, however it seems odd that I can pick an amount in lieu of dividing everything in half and giving them her half.I ask my accountant and to be honest I was as confused as I was after discussing it with my lawyer.Thank you,

A:

There is obviously a bit of miscommunication here, both with your attorney and your accountant. The transfer of ownership of the assets left behind by your wife is neither as simple as you are inferring from your attorney's comments, nor should it be as complicated as your accountant is making it out to be.

Each type of asset needs to be evaluated separately in regard to its taxability for the recipient, as well as its new stepped up basis for the recipient's records. You didn't say if you are in a community property state or not; but that fact is very important. If so, the entire cost basis of most of the assets is stepped up to its fair market value as of the date of your wife's death; while in non community property states, only the half owned by her is stepped up and your original half remains the same.

As your advisors should be explaining to you, most of the assets will pass with no tax consequence, with the main exception of the IRA accounts. Depending on what types of IRAs those are (conventional, non-deductible, Roth), they will most likely be taxable to the recipient, unless they are properly rolled over.

Your best bet would be to sit down with your legal and/or tax advisors and go over each item in your wife's estate individually and discuss these points. If neither of your advisors feels comfortable discussing these items in easy to understand terms rather than blanket generalizations, you will need to find a new advisor to work with; at least just for this matter.

I wish I could be more help, but that's all I can do for you at this time. Good luck.

Kerry Kerstetter

Labels: Estates

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/11/2007 12:21:00 PM Send this post:

Buy vs. Lease

Q:

Subject: Buy vs. Lease AnalysisKerry,I'm in the equipment leasing business and am constantly running up against our lease programs being compared to traditional bank financing. I believe leasing to be a better option in most cases because of banks "compensating balance" requirements and the fact that they usually place "blanket liens". In addition, Section 179 write-off vs MACRS depreciation also has real financial advantages. However many customers fail to take this into consideration, and instead focus solely on "interest rate".Have you ever put together a Buy vs Lease analysis template which could show the real after-tax cost of leasing vs traditional bank financing which will move the focus off of what banks are selling....interest rate...and give me real numbers instead of me attempting to explain the differences over the phone?

A:

I haven't designed my own such template because there are so many already available on the net for free, such as this one.

I haven't tested this one out for accuracy in real life situations, so you may want to run some tests before recommending it to your clients.

Good luck.

Kerry

Labels: Leasing

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/11/2007 12:18:00 PM Send this post:

Section 179 and Income Limits

Q:

Question about Section 179 Deduction

Dear Kerry - This is in response to an answer you posted regarding the ability to use Section 179 deduction amounts against wages.

1) If you have both business income and wage income, but the business income does not allow you to use the full Section 179 deduction, can you use the remaining dedution amount against wage income?

For instance, if you purchased an automobile for $10,000 and use it 50% for a business which you own, then you would have the right to a $5,000 section 179 deduction.

If however you could use only $2000 of this available deduction amount on Schedule C, then could you use the additional $3,000 as a deduction against wage income on Schedule A -- in the same year, same tax return?

2) As a separate but related question, if you cannot use the Section 179 deduction on Schedule C at all, are you required to use the available Section 179 deduction against wages in the same year the car was put into service... or can you carry the deduction forward to a Schedule C in a future year at your own discretion?

I hope that these questions are written clearly and I very much appreciate any advice you may have the time to offer!

With many thanks,

A:

The interplay between the allowable Section 179 deduction and the taxable income limitation is trickier than you think and is not the kind of analysis you should be doing on your own.

For example, the way the taxable income limit works is that it is very possible to have a Section 179 deduction create a large net loss on Schedule C. The actual deduction is required to be shown on the schedule for which the asset was used. In your case, if it was used for your Sch. C business, that is where the full allowable Section 179 would be shown, even though W-2 income may be what actually allows the deduction.

Another possible mis-statement that you need to clarify is the weight of the automobile. If it is under 6,000 pounds GVW, the allowable Section 179 deduction is much less than for a vehicle weighing more than that. Since you specified an automobile and not a truck or SUV, I wasn't sure you understood that important distinction, since most autos weigh much less than 6,000 pounds.

I hope this gives you the sense that you are in dangerous territory trying to do this kind of tax planning on your own. You should be working with a professional tax advisor who can show you with real numbers how such deductions would work out on your tax returns.

Good luck.

Kerry Kerstetter

Labels: 179

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/11/2007 12:13:00 PM Send this post:

Capital Gain or Ordinary Income?

From a Reader:

Since when is annuity income anything other than ordinary income under IRC Sec. 72 ? If there is capital gains treatment it's a new one to me. The typical deal on taking a lump sum from a deferred annuity is that the amount received net of any surrender charge less the amount invested in the contract is ordinary income shown on 1040 line 16b.

My Reply:

If the surrender of the annuity were reported on a 1099-R, you would be correct.

However, there were more assumptions contained in my analysis of the situation than I had time to explicitly spell out. My main one was that this was not a deferred comp retirement account that was being cashed in, but an investment vehicle sold by an insurance company that would have produced ordinary annuity income during its life.

When it was sold back to the insurance company, that would be treated as the sale of a capital asset, much like the sale of a stock or bond that also produces ordinary taxable dividend or interest income during its holding period.

I have actually had several real life cases of this kind of transaction with clients over the years. Reporting those sales (redemptions) on Schedule D never once created a problem with IRS; so this is more than just a theory on my part.

This is why it is so important for the taxpayer to have a tax professional review the actual transactions and the underlying documents to know with more certainty how something should be reported.

I hope this better clarifies my answer to that reader.

Thanks for writing.

Kerry Kerstetter

Labels: CapGains

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/11/2007 12:07:00 PM Send this post:

Mineral Lease Income

Q:

Subject: Lease Income

Kerry,If you had a mineral lease to receive payments as "rents", would you take payment as personal income and avoid the 15% SE tax, or structure a sole proprietorship/farm or LLC and receive it as income and take deductions? "Rents" are projected @ between 1K-6K/month for 8-12 years.I realize that there are potentially more deductions than the 15% SE, however I'm near retirement and don't want to do a business full-time.Also, to minimize liability, should I consider a family partnership/trust and sell or transfer the lease to it?Thanks for any insight you may give.

A:

This is the kind of thing that you really need to be addressing with your own personal professional tax advisor.

I'm not sure where you got the impression that the mineral lease payments would be subject to SE tax because that is not normally the case. SE tax would only be appropriate if you will be physically working to extract the minerals, such as with some gold miners I had as clients. However, if you are merely the property owner and are being paid for the use of the property, that income would be reported as Rent and/or Royalties on Schedule E, which is not subject to SE tax.

Whether there is a need to set up a separate entity for this or anything else in which you are involved is a subject nobody can competently comment on without detailed discussion and analysis of your unique circumstances.

Good luck. I hope this helps.

Kerry Kerstetter

Labels: Rentals

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/11/2007 12:00:00 PM Send this post:

Reduced Sec. 179 For Vehicles?

Q:

Subject: your comment about vehicles

Hello Kerry,In searching on the net for some credible comments about expensing 100% of movable business property, your website was the only one I found that seemed to have any straight forward comments. What I've found varies so widely, it all would go good with an Alice in Wonderland story. Also, what I've read (including on the IRS website) is that trucks with GVW over 6,000 had reverted back to a $2,600/yr max expensing, yet I had heard and read that the 100% (up to 100,000) had been extended, but all comments seem to be vauge at best. Other than your website, can't find much on this subject.Is per what you have posted on your website correct, that trucks with a GVW over 6,000 can still be expensed out in one year? Did the IRS/congress indeed extend this through 2009 or ?I found your website refreshing, as you seem to not beat around bushes. Also, it appears you are in Arkansas. Am looking to maybe find a state to live in where the real estate markets haven't gone out through the roof... Do you do CPA work in just a particular location in Arkansas? Does Arkansas have a personal income tax or corporate income/franchiese tax?Thanks!

A:

I'm not sure where that rumor started about the reduction in the vehicle Section 179, but that's completely bogus. As I've explained several times, the 6,000 pound exception to the Luxury Vehicle rule has been around since 1984 and has never been repealed.

I have a lot of info on Section 179 on my website.

As I frequently explain to people who ask me to prove that a certain item of tax law hasn't been changed, it's difficult to prove a negative (that something hasn't happened) and I don't have time to debunk every crazy tax rumor that's floating around. The burden of proof should be on those who claim that something has changed. Make those people who are telling you that the law has been changed prove their statements

Arkansas does have an income tax on both individuals and corporations. You can see the rates and other details on the DFA's website.

As you can see in my email signature, I haven't been accepting any new clients for a number of years and don't know if or when I will take any new ones on.

Good luck. I hope this helps.

Kerry Kerstetter

Follow-Up:

Hello Kerry,I can see why you're booked up. Your web page below is very clear and straight forward. I'm amazed from what I found on many other "tax" sites and even when searching the IRS website about this, what I found was that for vehicles over 6,000 GVW, the yearly maximum had reverted back to something like 2,600, and yes, I kept trying to make sure I was searching for trucks, not SUV's. It's hard to find competent and knowledgable tax accountants. Appreciate the feedback and best wishes.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/11/2007 11:54:00 AM Send this post:

Petraeus Caves to Dems, Orders Surge of Accountants – Another funny parody from Scott Ott.

Labels: humor

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/10/2007 12:55:00 PM Send this post:

Dianetics, the Tax Plan – Bruce Bartlett isn’t slowing down in his attempts to discredit the FairTax by trying to associate it with Scientology. It’s a bit of a stretch to claim that just because the Church of Scientology didn’t like the IRS and proposed ways to abolish that agency, that anyone who also proposes doing away with IRS is a fellow space traveler with the likes of John Travolta and Tom Cruise. I would hazard a bet that if Americans were polled on what agencies they would like to see eliminated, IRS would be at the very top. Does that make everyone who wants to say goodbye to IRS a Scientologist?

Labels: FairTax

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/07/2007 10:16:00 PM Send this post:

No Change in the IRS Interest Rates for the Fourth Quarter of 2007 - Still at the same 8.0% rate that was set as of 7/1/06. I’ve updated this on the Quick Reference page of my main website.

Labels: IRS

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/04/2007 03:40:00 PM Send this post:

Email Tax Scams

Snopes.com has these notices about recent fake IRS emails floating around trying to obtain personal info from unsuspecting folks, aka phishing. I haven’t received any of these myself because I am a strict user of MailWasher to purge my email accounts of spam and scams before bring anything into my main Eudora email; but I have received some emails from readers who did receive some of these fake IRS emails.

E-mail from the IRS offers $80 to those who complete "member satisfaction surveys.

E-mailed IRS notice claims the recipient is eligible for a tax refund.

IRS has also put out another news release on these kinds of scams.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/01/2007 02:47:00 PM Send this post: