![]()

Useful WebSites:

April 1999

July 2000

November 2000

December 2000

January 2001

February 2001

March 2001

April 2001

May 2001

June 2001

July 2001

August 2001

September 2001

October 2001

November 2001

December 2001

January 2002

February 2002

March 2002

April 2002

May 2002

June 2002

July 2002

August 2002

September 2002

October 2002

November 2002

December 2002

January 2003

February 2003

March 2003

April 2003

May 2003

June 2003

July 2003

August 2003

September 2003

October 2003

November 2003

December 2003

January 2004

February 2004

March 2004

April 2004

May 2004

June 2004

July 2004

August 2004

September 2004

October 2004

November 2004

December 2004

January 2005

February 2005

March 2005

April 2005

May 2005

June 2005

July 2005

August 2005

September 2005

October 2005

November 2005

December 2005

January 2006

February 2006

March 2006

April 2006

May 2006

June 2006

July 2006

August 2006

September 2006

October 2006

November 2006

December 2006

January 2007

February 2007

March 2007

April 2007

May 2007

June 2007

July 2007

August 2007

September 2007

October 2007

November 2007

December 2007

January 2008

February 2008

March 2008

April 2008

May 2008

June 2008

July 2008

August 2008

September 2008

October 2008

November 2008

December 2008

January 2009

February 2009

March 2009

April 2009

May 2009

June 2009

July 2009

August 2009

September 2009

October 2009

November 2009

December 2009

January 2010

February 2010

March 2010

Selling Two Residences

Each taxpayer can only have one primary residence at a time. However, if a married couple can prove that they lived in separate homes, a couple can have two primary residences, as discussed in this vidcast.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 12/17/2009 06:38:00 PM Send this post:

Changes to tax free home sale rules?

Q:

Subject: Sale of Primary Residence

I am trying to find out when the $500,000 ($250,000 per spouse) Exclusion expires; and what is the current thinking on how it would be changed.

Sincerely

A:

The current law allowing the tax free exclusion of some or all of the gain from the sale of a primary residence (aka Section 121) was enacted in May 1997 and does not have an expiration date. It will be the law, with the exact same dollar amounts (unadjusted for inflation) until our rulers in DC explicitly change it.

While nobody can know for sure what changes, if any, this law will have in the future, I can guess at a few possible ones. It is very likely that some provisions of this law will be trimmed back for home sellers.

Going back to a once in a lifetime usage, rather than the current once every two years, would probably be a politically acceptable change since that was how it applied for several decades prior to 1997.

Another likely change with the growing sentiment in DC to screw over the evil rich would be to completely or partially deny the exemption to those taxpayers with AGIs over a certain dollar figure that our rulers will establish to define them as evil rich who are unworthy of any more tax breaks. Several other tax deductions and credits already have AGI eligibility thresholds; so this would be consistent with that.

Your own personal professional tax advisor should be up on the latest laws in regard to home sales; so any planned sale should be run by him/her first.

I hope this helps. Good luck.

Kerry Kerstetter

Follow-Up:

Dear Kerry

Thank you so very much for the information ... it is extremely helpful

Sincerely

Labels: 121

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/15/2009 08:11:00 PM Send this post:

Selling Vacant Land

Q:

Subject: Vacant Land

If I sale my vacant land and meet all requirements can I still take an Exclusion on the land without the sale of my residence? Still confused about the tax law/ publication #523 any response would be greatly appreciated! Thanks

A:

You didn't say if the vacant land was connected to your primary residence or not.

I have a section on this topic on my page on home sales.

Unless you are planing to sell your home within two years of the separate sale of adjoining bare land, it will not qualify for any exclusion of gain.

You really need to be working with a professional tax advisor to see if there will even be any capital gains taxes on the land sale. There is a special zero percent tax on some gains for some people in 2009 and 2010 that you might be able to utilize.

Good luck.

Kerry Kerstetter

Follow-Up:

KERRY, Yes the vacant land is connected to my primary residence. Thank you for the current reply.

Labels: 121

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 3/09/2009 05:42:00 PM Send this post:

Prorated Home Sale Exclusion

Q:

Subject: Home Sale Gain Exclusion

Situation:

5 years ago, was laid off in Minnesota and had to settle for a California job.

Commuted every 2 weeks for 1 year then moved family to a rental.

Wife and children lived in MN home every time children not in school (about 3 months per year), nevertheless total days is well shy of 730.Kept a car registered in MN, voted in MN, kept MN drivers licenses, bank account in MN while trying unsuccessfully to transition to a job back in Minnesota. Even had several in-person interviews in MN over the years.

Finally gave up & sold in Minnesota; just closed. We expected to exclude 50K of gain.

Can we

A) Exclude the gain because our beloved MN home was our primary residence defined by that we never bought anything else and always considered & treated it as "our home".

B) Exclude the gain because the wife was always staying there... it may be shy of 730 days but there is no way to audit that.

C) Exclude the gain because I was forced to sell due to a job situation and we used it as a primary residence for 1 year, 50% of the 2 year standard, and all we need to exclude is $25K apiece.

D) SOLThanks!

A:

You need to be working with an experienced professional tax advisor to make sure you do things properly here.

It looks like you should be able to qualify for the prorated tax free exclusion based on your change in employment. Since your gain is only 10% of the total possible Section l21 exclusion of $500,000, there shouldn't be a problem in excluding the full amount of your profit.

However, your personal professional tax advisor will be better able to evaluate the details of your situation and decide if that is the case.

Good luck.

Kerry Kerstetter

Labels: 121

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 2/14/2009 12:07:00 PM Send this post:

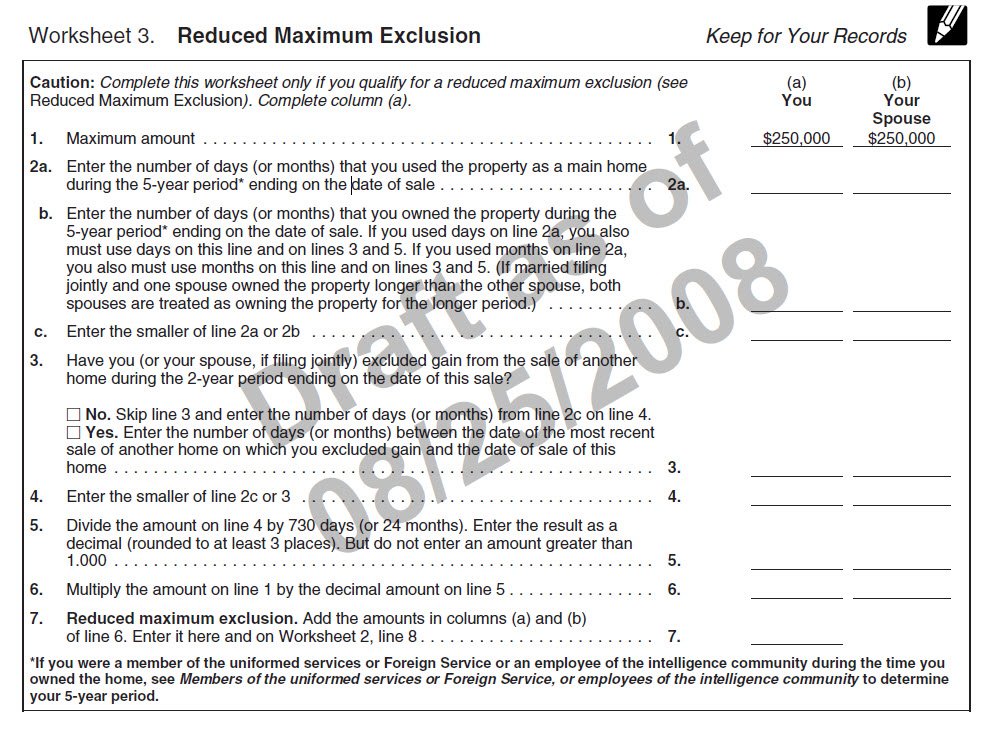

Reduced Sec 121 Exclusion Worksheet

As I was perusing the latest draft tax forms on the IRS website, I came across this file that contains some new worksheets and other info for Publication 523, which deals with the tax free sales of primary residences.

What I was mainly interested in is the brand new provision in the law that limits the tax free exclusion for homes that were also used as a rental or second personal home. For that calculation, IRS has this new worksheet, which is on Page 7 of the draft pdf file.

(Click on image for full size)

Labels: 121

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/04/2008 02:16:00 PM Send this post:

Income Gain Exclusions – The Scoop on Code Sec. 121 – From TrustMakers, including the newly passed change.

Labels: 121

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 8/12/2008 08:25:00 PM Send this post:

Tax Break on Capital Gains Narrows - More details on the new changes to the tax free home sale rules.

Labels: 121

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 8/11/2008 03:05:00 PM Send this post:

The new tax law changes

As always, our rulers in DC have screwed up any attempt at tax simplification with yet another new law changing the rules of the game.

Here are some highlights of the new tax related changes courtesy of one of my favorite reference sources, TaxCoach Software:

On Wednesday, July 30, President Bush signed the "Housing and Economic Recovery Act of 2008." While the bill focuses on protecting lenders and preventing foreclosures, there are three other tax provisions worth noting.

1. The 2008 Housing Act gives “first-time homebuyers” (those who have not owned a primary residence for three years) a tax “credit” equal to 10% of the new home’s purchase price, up to $7,500 ($3,750 for married couples filing separately). This “credit” is available for purchases from April 9, 2008 through June 30, 2009. But, if you take the credit, you have to pay it back, in equal installments, over the next 15 years. So it’s really just an interest-free loan, not a true tax credit. It phases out for incomes between $75,000 and $95,000 ($150,000 and $170,000 for joint filers).2. The law creates a temporary deduction, for 2008 only, for property taxes for non-itemizers. The deduction is limited to $500 ($1,000 for married couples filing jointly).

3. The law eliminates tax breaks on the sale of your principal residence for periods you don't use it as your principal residence. Under old law, you could take a rental property or vacation home, use it for at least two years as your primary residence (five years if you acquired it in a Section 1031 exchange), then sell it and exclude up to $250,000 of gain from your income ($500,000 for married couples filing jointly). This held true even if most of the gain occurred while you were renting the property or using it as a vacation home. The new law taxes you on any gain after 2008 attributable to periods you don't use it as your primary residence. (There’s no need to appraise the property to determine interim value; the new law determines excluded appreciation on a pro-rata basis, according to how long you own it.)

Labels: 121, Credits, PropertyTax

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/31/2008 06:50:00 PM Send this post:

Retroactive home sale?

Q:

Subject: Sale of residence

I am a tax preparer with a small office in MI and am wondering if you would give me your opinion on a transaction. I have a client who leased a former residence to someone for up to five years, with an option to buy at any time during the lease period. The buyer/tenant assumed all practical ownership responsibilities for maintenance, paid a higher than market rent during the 5 years so that a portion of the rent was applied to the option sale price and a portion of the "rent" was designated as property tax and insurance reimbursement. The buyer was trying to work out of some personal tax liens and they took most of the five years to do so. My client did not want to sell on a land contract because it would be harder to evict the buyer if the personal tax issues could not be resolved and third party financing obtained. The sale was completed in 2007.

My client, the seller, received a 1099 for the 2007 closing and they would like to exclude the gain on sale, other than depreciation recapture. Their contention is they really sold the property in 2001 when the lease/option started. The lease payment was equal to a reasonable interest rate, plus tax and insurance escrow and the amount applied to the down payment amount. While the title did not transfer in 2001, the client's contention is there was basically a land contract sale in 2001, at which time they met the ownership and occupancy requirements. All payments received during the almost five year period have been reported as rent and the property was depreciated- perhaps not the right thing to do (in hind sight).

I have not found anything right on point so I am wondering if you would give me your thoughts on this. Thanks for taking the time to read this and I look forward to reading your response

A:

I am assuming that your client didn't report the sale of his primary residence, with the Section 121 tax free exclusion, on his 2001 1040, which is where it should have been shown if he wanted to claim it as such. Trying to recategorize the sale from a normal lease-option (which it seems like to me) to a primary residence sale six years after the fact, when the statute of limitations bars any changes to his 2001 1040, is crazy and not something that would have any chance of standing up to the slightest bit of IRS scrutiny.

In addition, if he has been claiming depreciation since 2001, that also completely undermines his argument that he actually sold the property back then. Having his cake and eating it too seems to fit that scenario.

I am also assuming that your client hadn't been reporting any interest income from the buyer's payments; another contradiction to the argument that there was a 2001 sale.

Based on your description, your client had a standard lease option with a 2007 sale of a rental property. He could have obviously done a 1031 exchange into new rental property during 2007, but it is too late now to make that kind of change in the type of transaction he had.

If you've read much of my postings, you know that I have very little sympathy for people who are too short sighted and/or cheap to consult with a professional tax advisor before the consummation of a potentially taxable transaction and then cry about the consequences when their 1040 is prepared. The proper time for your client to consult with you would have been before the 2007 closing of the sale. You may have advised to set it up as a 1031 exchange or even as an installment sale if he could have afforded to carry back some of the sales price. Now, it is too late to set those things up and he has a fully taxable sale of a rental property.

That's how I see it. I hope this helps.

Kerry Kerstetter

Labels: 121

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 6/26/2008 02:56:00 PM Send this post:

Multiple primary residences?

Q:

Subject: claim multiple primary residences

I have been told that people are able to claim multiple primary residences, since we did not use a second property as a second home. In fact we used it as our primary residence 2 or 3 days a week on the average, due to operation of the business in another town, for the last 5-6 years; not vacationing.Thanks,

A:

You appear to be mixing up the issue of multiple primary residences. At any point in time, each person can only have one primary residence for IRS purposes based on such items as time spent, mailing address, voter registration, driver's license, etc.

With a married couple, it may be possible for each spouse to have his/her own primary residence if they do in fact live in separate locations. As with all tax matters, the burden of proving the legitimacy of such a classification rests with the taxpayers. IRS does not have to prove it it isn't valid. You have to be able to prove that each spouse has his/her own separate primary residence.

Where you may be confused is the fact that each taxpayers is allowed to exclude up to $250,000 of profit from the sale of a primary residence each two years. Before May 1997, the tax law had included a once in a lifetime exclusion of gain from a primary residence sale. The liberalization of the law to allow multiple usage of this tax free break has been a great opportunity for tax free serial home selling, such as with rental properties that are converted into primary residences.

I have some info on home sales on my website.

Before undertaking any transaction related to this area of taxation, you should consult with a professional tax advisor.

I hope this helps.

Good luck.

Kerry Kerstetter

Labels: 121

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 6/19/2008 09:18:00 AM Send this post:

Tax free home sale?

Q:

Subject: Buying a new home, 2 tax questions

1) is the sale of my current home a tax-exempt event? We’re in our 40’s and are moving to a larger house (if any of that affects the answer)

2) at closing, the sellers will bring prop taxes up to date (a little over a year’s worth of taxes). Shortly after that, spring 08 taxes will be due and paid by us. Do we get to deduct that property tax payment on Schedule A? Do the taxes they gave us at closing to get current count as income or offset the prop tax payment?

Thx

A:

Whether any or all of the gain on your home sale is taxable will depend on a number of factors that you need to review with your own personal professional tax advisor.

To get yourself up to speed on the rules, you should check out this article on the rules for home sales.

You will see that both your age and your plans to buy a new home are completely irrelevant to the taxability issue.

Settlement statements from both property purchases and sales are filled with tax deductible items, such as loan costs and property taxes. This is why any good professional tax advisor will request that you supply him/her with copies of those statements. S/he will know who to report the prorated taxes.

I hope this helps. Good luck.

Kerry Kerstetter

Follow-Up:

Thx for the quick response!

Labels: 121

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 5/21/2008 02:02:00 PM Send this post:

Reduced tax free gain on home sale...

Q:

I came across your information on the web and was wondering if you could clarify what the pro-rated capital gains exclusion (amount) is for selling your primary residence less then 2 years. Is this $342.47 per day, per person for the length of time that you lived in the house before selling?

I would be happy to compensate you for your advice.

Thanks

A:

The tax free gain does work out be $342.46 per day that you both owned and lived in the home as your primary residence. This is $250,000 divided by 730 days.

IRS has a worksheet for calculating the reduced excludable gain in Publication 523 on their website.

Most professional tax software has the capability to calculate this based on the number of qualifying days; so be sure to give that figure to your personal professional tax preparer.

Good luck.

Kerry Kerstetter

Labels: 121

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 4/23/2008 07:38:00 PM Send this post:

Assuming someone else's Sec. 121 eligibililty?

Q:

Subject: 1031 question

Hello,

I know you deal in the 1031 exchange field and I also know from reading your blog your deal with tax issues in a liberal reading. So I feel you are a good person to get an open minded view from.Is there a way to use someone else's 2 out of 5 years? Drew Miles, Tax Attorney claims there is a way/program to do this. Is this something you have heard about? Can you guide me to some references.

Thanks,

A:

The only way I am aware of for one person to benefit from someone else's time in a home in terms of qualifying for the $500,000 tax free exclusion, is with spouses. IRS allows the full exclusion if either spouse owns the home for at least two out of the previous five years. However, they require both spouses to use the home as their primary residence in order to exclude the full $500,000. Shorter times as a residence by each spouse would require prorated adjustments in the excludable gain.

In regard to being able to walk in and assume the tax benefits of an unrelated person's use of a home as if they were yours, I don't see how that is possible.

I checked Drew Miles' various websites and see nothing other than his vague promises of tax savings secrets, with no mention of this issue. I would be interested in seeing what you are referring to before concluding that you are misreading it.

Kerry Kerstetter

Labels: 121

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 4/03/2008 09:50:00 AM Send this post:

Possible Dem Tax Hikes?

Q:

Subject: Primary residence tax question

This morning I was speaking to a friend who is a local REALTOR. She is suggesting that some people seem to be under the impression that if the Democrats win this election, this tax law could be changed or eliminated. What is your impression or awares on this subject.Thank you for your time,

A:

If you're referring to the Section 121 $250,000 tax free gain rule, I haven't noticed any discussion of anyone suggesting repealing this.

The Dems are seriously discussing several other huge tax hikes, such as allowing the Bush tax cuts to expire in a few years, removing the special lower tax rates for long term capital gains, and no repeal of the Estate Tax.

As I posted in my blog recently, in California, the Dems are attempting to remove the deduction for home mortgage interest, which could be an indication of how DC Dems might move. There's always a chance that they could scale back the limit on how large deductible home mortgages could be from the current million dollar level.

It's all speculation and conjecture at this point, but as much as I fear the Dems' tax hiking urges, I'm not very worried about them removing the tax free home sale rule. Luckily, it's not part of the Bush temporary tax cuts, so it will live on until enough of our rulers in DC decide to attack it.

Worst case scenario that I could imagine would be for them to scale its savings opportunities back a bit, such as by making it a once in a lifetime deal, as the previous law was, instead of the current ability to use it every two years.

There's also the possibility that they could reduce the amount of tax free gain from the $250,000 per person level. However, since that amount was established in 1997 and has no provisions for any inflation adjustments, I don't see that happening either.

That's how I see it. Thanks for writing.

Kerry Kerstetter

Labels: 121

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 3/30/2008 04:29:00 PM Send this post:

Counting days occupying primary residence...

Q:

We owned our home for more than five years and had it rented until 9/1/05 when it become our primary residence? The IRS is asking us how many days we lived in California? Before I put the answer on my tax form I would like to know if we spent approximately tow month traveling to our second home in Texas will it disqualify us for the exclusion? We had to sell the home because of financial reasons. This property become our primary residence on 9/1/05 to 11/8/07. We had all our mail there, utility bills, bank accounts and registered to vote. Thank you for your help as I am worried about this.

A:

You really need to be working directly with a tax pro to make sure everything is handled properly rather than trying to work through the rules on your own.

You are obviously trying to see if you qualify for the ownership and occupancy test of two out of the previous five years in order to be able to qualify for the full tax free exclusion. You seem to be confused as to whether visiting your second home doesn't allow you to count that time as part of your time in the primary home.

As any competent professional tax advisor should be able to tell you, the occupancy rule doesn't require that you actually be physically present in that house for 24 hours of every single day or even every single day that you are counting. Real life for most people does include time spent away from their main home for various reasons, be they business, medical or purely personal. As long as your primary residence is still considered your main base of operations, time you spend away temporarily at another location, including your own second home in another state, shouldn't count against you. As long as you don't take any of the steps to change your official primary residency away from the one you have had, you should be able to count that time as part of your ownership and occupancy.

Besides dealing with this issue, you will also need the assistance of a good tax professional to help you calculate the proper adjusted cost basis of your old home, including adjusting it for deprecation, to see if the exclusion will be enough to cover your paper gain.

Good luck.

Kerry Kerstetter

Follow-Up 1:

Thank you for your reply. I will contact a CPA and have him do our taxes. I appreciate your advise. The only reason that I became paranoid is the form ask" how many days did you spend in California." We spent two years less about 90 days that we spent in our second home.

Follow-Up 2:

Thank you for your time in answering my question. I have made an appointment with a CPA.

Sincerely,

Labels: 121

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 2/20/2008 05:35:00 PM Send this post:

Condo Sale...

Q:

Subject: capital gains dilemma

I'm not sure if you answer questions or not but I'll shoot an quick email to find out.I have a question on capital gains. I bought a condo in Boston in 1998 and lived in my condo until January 2006 in which I started to rent it. Since then I got married and we bought a house in June 2006. Even though we both work our mortgage is high and money is too tight and am considering selling my condo to put towards our mortgage to reduce payments.I am trying to learn about capital gains and have read if you live in your property that you are selling for 2 of the 5 years before the sale you would not have to pay capital gains. Can you tell me if I am eligible to avoid capital gains.Thank you,

A:

You should qualify for up to $250,000 of tax free gain, and possibly a little more for your husband on a joint 1040. A little twist will be the recapture of depreciation claimed on the condo during its use as a rental.

I have a lot of the details explained on my website.

You should go over the specifics of your unique situation with your own personal professional tax advisor.

Good luck. I hope this helps.

Kerry Kerstetter

Labels: 121

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/08/2007 07:10:00 PM Send this post:

Special IRS Web Section Unveiled for Homeowners Who Lose Homes; Foreclosure Tax Relief Available to Many - Here is a direct link to the IRS FAQ page on foreclosures.

As I’ve said before, this entire issue is being blown way out of proportion in regard to its negative tax consequences. Most people who suffer foreclosures will either have nondeductible losses or be more than covered by the Section 121 tax free exclusion.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 9/19/2007 09:59:00 PM Send this post:

Sec. 1031 & 121

Q:

Subject: Exchange QuestionWe are considering doing a 1031 exchange on a single family rental, which has been held for 32 years, and is owned free and clear.The idea would be to exchange this rental home for TWO single family homes, and use them as rentals (like/kind). Then, after 3 years, move into one of the rentals and live in it for two years, meeting the five year holding requirement & 2 year residency requirement .... Then we would sell new Rental Property #1 as a personal residence, and then move into the Rental Property #2 as a permanent residence, and live in it indefinitely.Each of the newly exchanged properties would be rentals - the first one for 3 years (then move in for 2 years), for a total of 5 ... and the next exchange property would be a rental for 5 years until we could meet the time requirements.This is hard for me to explain, but I hope you can get a grasp of what I'm trying to do. Trade one rental for two, and live in the two rentals (over a period of five years before moving into rental #2) so as not to pay capital gain taxes. Would these time lines work?

A:

That plan could work, assuming our rulers in DC don't mess with the tax laws over the next five years to change any of the timing details, which you have correct for the laws as they stand now.

I have one very big word of caution for you. Keep your intention to reside in one of the new rentals to yourself. Blabbing around to a lot of people that you had that plan from the beginning could jeopardize your 1031 exchange because an aggressive IRS agent could classify the house as personal at the time of the exchange. I have seen and heard of cases where people shot themselves in the foot by bragging about plans such as yours. All it takes is one jealous person to turn you in and you're cooked. The decision to move into the rental has to appear to be made long after you take ownership of it.

Other than that, it sounds as if you are looking at things creatively, which is what makes the tax game so much fun.

Good luck.

Kerry Kerstetter

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 5/15/2007 11:11:00 AM Send this post:

Jointly Owned Property

Q:

Subject: Sale of home question

Hi Tax Guru,

Found your website while browsing for an answer to my question about a sale of a home I own with my parents. Here's the situation:

Here are the circumstances:

My brother and I own a property with my parents. We are all on title as joint tenants (1/4 undivided interest to each of us and 50% undivided interest to my parents). The house was bought in 2000, my parents supplied the down and my brother and I have payed for the mortgage and taxes since. We've split the deductions every year between the two of us. My parents have used this as their primary residence since 2000 while my brother and I do not. We have considered it our 2nd home as we each own our own primary residence. We are now interested in selling the home and are wondering what is the best way to reduce the tax implications for everyone. I estimate the capital gains on the home to be approximately 300K.

Since my parents use it as their primary residence, would they be able to "claim" all the capital gains (300K) or do the gains have to be divided equally among the 4 owners? If it has to be divided, is there any way to get off the title so that my parents can take advantage 500K exemption without triggering gift tax consequences for my brother and I? Any suggestions on how we can either structure the title or the sale such that taxes are minimized for all parties? My parents income is low while my brother and I are in much higher brackets if we had to pay taxes.

Appreciate any insight you might have on mitigating the tax burden.

Thanks very much!

A:

This is an issue that you all really need to work on with the assistance of an experienced professional tax advisor because there are a number of ways in which it can be handled and several factors that need to be considered, such as the following.

It is obvious that your parents can qualify for the Section 121 tax free exclusion of the gain on their one half of the home's net gain. The gain on the half that you and your bother own is a much more complicated issue.

Let me address the gifting option. You and your brother could gift your shares of the home to your parents. However, this would require you both to file gift tax returns to report it and either pay gift tax or use up part of your million dollar lifetime exclusion. Your parents would assume your cost basis in the 50% of the home they are given and would essentially be accepting full responsibility for your and your brother's gain.

The half of the home that your parents are given will not qualify for the Section 121 tax free exclusion because the law requires the seller to both own and occupy it is their primary residence. While your parents have obviously met the occupied test, they would fail the ownership test and would thus be required to report the gain on their "new" 50% share as taxable long term capital gain (LTCG). Because they had been using all of the home for personal purposes, its sale cannot be structured as a Section 1031 like kind exchange, which is only available for business and investment property.

If you and your brother keep your share of the house, the gain is potentially taxable, depending on how you and he are classifying its ownership, which should be consistent with how you have been reporting the deductions for interest and property taxes on your 1040s.

If you have been treating the home as investment property, you can structure your disposal of your share of the home as a Section 1031 like kind exchange, which will require you to use the services of a neutral third party facilitator to reinvest the proceeds into new (to you) business or investment property within 180 days. These rules are all explained at tfec.com.

If you have been reflecting that you have been personally using the home, it will not qualify for Section 1031 and you will have a taxable LTCG.

You and your brother don't necessarily have to report this in exactly the same way. The strategy for each of you and your brother could be different depending on your unique situations. For example, one of you may qualify for a Section 1031 exchange, while the other may not.

The actual tax hit on any taxable gain could be spread out over several years under the installment method if part or all of the sales price is carried back. Your personal professional tax advisor can show you how that would work with your numbers and sales terms.

I hope this gives you some idea of the various details that you all need to be evaluating with your personal professional tax advisors.

Good luck.

Kerry Kerstetter

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 5/06/2007 06:59:00 PM Send this post: